INVESTING

By Herbert Lash and Marc Jones

NEW YORK/LONDON (Reuters) – A gauge of global equities edged lower and the dollar inched up on Tuesday as markets awaited word from the Federal Reserve chief after last week’s blockbuster U.S. jobs number made clear interest rates will stay higher for longer to combat inflation.

The Australian dollar earlier bolted higher after its central bank reiterated further increases would be needed, while the yen gained after an unusually strong Japanese wage data.

U.S. and European equity markets were mixed to lower, with the euro and pound lower against the dollar. The broad pan-European STOXX 600 index was up 0.04% and MSCI’s gauge of global stock performance shed 0.12%.

The spotlight was on central bankers, especially Fed Chief Jerome Powell, scheduled to speak at noon (1700 GMT), as stronger economic data pointed to more stubborn inflation.

The U.S. economy is getting more attention because of Friday’s payrolls number – almost three times greater than market expectations – and because of the upgrades in hiring over the past few months, said Joe Manimbo, senior market analyst at Convera in Washington.

The market now see the Fed with the upper hand in terms of remaining on this hawkish path,” Manimbo said. What’s been really important is that the market sees a lower likelihood of rate cuts by the end of the year.”

An ECB survey on Tuesday showed euro zone inflation expectations were still edging up at the end of last year, while Fed Minneapolis President Neel Kashkari said he still thought the U.S. overnight lending rates should rise to at least 5.4% from 4.5%-4.75% range.

Nobody should over react to one report,” he said, referring to Friday’s payrolls data, but he also noted the services sector remained very robust.

On Wall Street, the Dow Jones Industrial Average fell 0.34%, the S&P 500 lost 0.18% and the Nasdaq Composite added 0.03%.

Asian stocks stabilized overnight after they, like most global share markets, suffered steep losses following that U.S jobs data.

MSCI’s broadest index of Asia-Pacific shares outside Japan ended up 0.2%, but Australia’s S&P/ASX200 slipped nearly 0.5% after the Reserve Bank of Australia delivered its ninth consecutive rate hike. Australia’s cash rate now stands at 3.35%, a decade high.

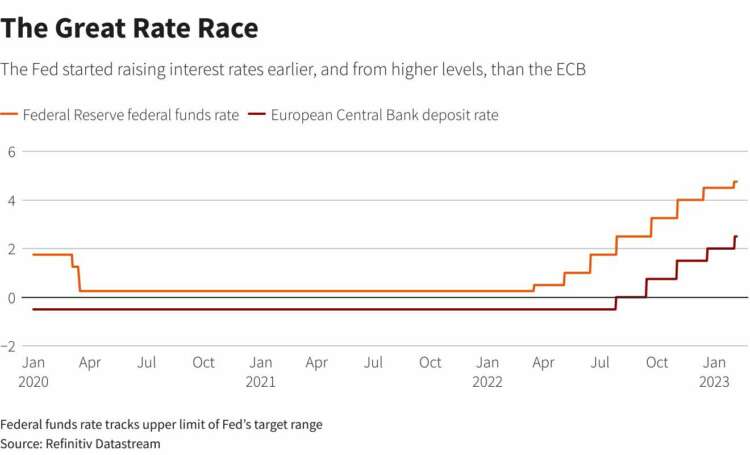

Graphic: The Great Rate Race- https://www.reuters.com/graphics/BRV-BRV/xmpjkrbmgvr/chart.png

DEADLY QUAKE

U.S. stock index futures edged higher ahead of the start of trading in New York. Fed’s Powell’s is due to speak at 12:40 p.m. EST (1740 GMT) while President Joe Biden will deliver his second State of the Union address at about 9 p.m. (0200 GMT Wednesday).

The speech will give Biden a chance to shape public perception of the debt ceiling, social spending, the Russian war in Ukraine and tensions with China.

Another major move in markets was oil’s jump for a second straight session on optimism about recovering demand from China and supply concerns following the shutdown of a major export terminal after an earthquake in Turkey.

U.S. crude recently rose 1.54% to $75.25 per barrel and Brent was at $81.84, up 1.05% on the day.

In the bond markets, benchmark government bond yields crept higher, with the 10-year German Bund trading at 2.32%, compared to less than 2% three weeks ago and the benchmark 10-year Treasury note was at 3.65%.

Italy’s 10-year yield was up around 5 basis points on the day at 4.197%, leaving the closely watched gap between Italy and German at around 185 bps.

Sentiment in markets is dominated by central banks and the repricing of rates yet again,” Kerry Craig, JPMorgan Asset Management’s global market strategist, said.

(Reporting by Herbert Lash, additional reporting by Marc Jones in London, Scoot Murdoch in Sydney; Editing by Jacqueline Wong, Tomasz Janowski and Arun Koyyur)

-

-

BUSINESS4 days ago

BUSINESS4 days agoBuilding a Diverse and Inclusive Team in Your Startup

-

-

-

FINANCE4 days ago

Changelly launches Probably Serious Quiz introducing 0% fee swaps of USDt on TON and Toncoin

-

-

-

BUSINESS3 days ago

Essential Strategies for Startup Bootstrapping and Financial Management

-

-

-

NEWS4 days ago

Global equity market-neutral hedge funds shine

-